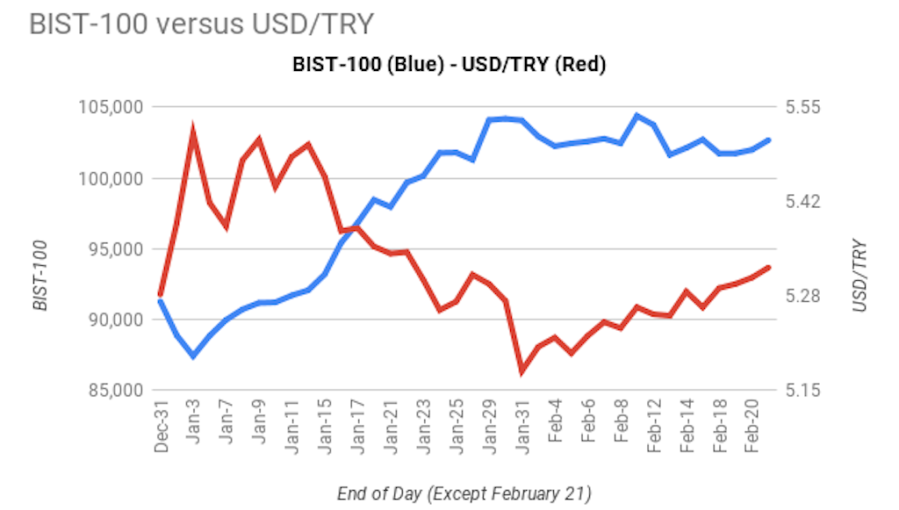

Turkey’s stock market has returned 52% since last August as it recovers from a deep plunge caused by last year’s currency crisis. But now investors are starting to wonder if the recovery rally has run its course.

VTB Capital downgraded Turkish equities to equal weight from overweight in emerging markets although it is still relatively more upbeat on banks than non-financials in Turkey portfolios, Akin Tuzun of the Russian investment bank said on February 19 in a research note entitled “Turkish Equities – Taking profits in overweight positions”.

The Turkish equity market has risen 52% in dollar terms since its lows in August, and outperformed the EM/EMEA space by 55%. VTB Capital was bullish in 3Q18, upgrading Turkey and Turkish banks to a strong buy; however, it now sees the risk-reward as more balanced.

On February 21, the central bank said in its regular weekly bulletin that total outflows from Turkish equities amounted to $169mn in the first half of February versus an inflow of $1.34bn in January while outflows from domestic government debt securities stood at $308mn between February 1 and February 15, bringing total outflows so far this year to $638mn.

Bank rally over

In a separate research note entitled “Turkish Banks – Time to take a breather” published also on February 19, Tuzun said that VTB Capital revised its view on Turkish banking sector to Neutral from Strong Buy.

Following the restructuring of the bank sector after the 2001 crisis the sector became a favourite of investors and remains strong to this day. Turkish banks rallied 78% in dollar terms from their lows in August, and outperformed global EM and EMEA financials by 70% and 68%, respectively.

After the rally of the last five months VTB cut Akbank, Garanti Bank, Halkbank and Isbank to Hold from Buy but it still keeps Vakifbank and Yapi Kredi Bank at Buy. The investment bank expects high volatility in 2019.

The share of foreign investors in the free float of Borsa Istanbul has risen back to its highs of the past five years. Thus, the market is no longer under-owned by foreign institutional investors, which caps further upside risks, VTB Capital believes.

Some industrials still attractive

VTB Capital also believes it is time to trade again in Turkish equities. Although it is in its ‘neutral’ territory for various metrics, it believes that there will be attractive trading opportunities for Turkish assets in 2019.

According to a separate research note on Turkish energy industry published on February 20, VTB increased its 12-month target price for Tupras (Buy) to TRY 164 and lowered its target for Aygaz (Hold) to TRY12.3.

On February 21, Vladimir Bespalov of VTB Capital said in a research note on Turkish cementmaker Cimsa’s Q4 financials entitled “Weak financials support our cautious view” that VTB reiterates its Hold advise for Cimsa with a 12-month target price of TRY8.

Cimsa reported a net loss of TRY62mn for Q4 vs. the TRY 11mn net profit suggested by the consensus. Although white cement exports provide a certain cushion, VTB believes that Cimsa faces strong headwinds domestically.

On February 21, Turkish statistical institute TUIK said that Turkey’s construction cost index fell, for the third consecutive month, to 25.65% in December from its peak of 39.66% in August. On February 19, TUIK said that number of buildings, floor area of buildings, value of buildings and number of dwelling units given construction permits in 2018 decreased by 36.7% y/y, 48.9% y/y, 35.8% y/y and 53.3% y/y, respectively. On February 18, TUIK said that the number of homes sold in Turkey declined by 25% y/y in January with mortgage sales shrinking 77% y/y. Also on February 18, the central bank said that home prices in Turkey rose by a limited 9.69% y/y in December versus a CPI inflation of 20.3% y/y.

On February 15, Bespalov said in a note on carmaker Tofas’ TRY1.6 per share dividend announcement, which implies a 9.5% yield, that VTB reiterated Buy advice with a 12-month target price of TRY30.

Tacirler Invest also maintains its BUY rating for Tofas, Ece Mandaci of Istanbul-based brokerage house said on February 19 in a research note.

Also on February 15, Bespalov said in an earning release on Turkish auto retailer Dogus Otomotiv entitled “4Q18; positive, but leverage and outlook remain a concern” that VTB reiterated its Hold advice on Dogus with a 12-month target price of TRY5.50.

Telecoms and retail cut to hold

On February 21, Ivan Kim of VTB Capital said in a research note on Turkey’s largest mobile operator Turkcell that VTB cut Turkcell to Hold from Buy, given a 12-month target price of TRY16.

Post the 48% dollar-terms gain since the beginning of 3Q18 (86% from early September), VTB believes that Turkcell might take a breather.

Turkcell is facing a more challenging year, the 4Q18 slowdown points to downside risks to mobile service revenue performance in 2019, Kim said, adding that Turkcell’s balance sheet remains strong, with the net long FX position post the Fintur sale.

Turkcell said on February 20 in a bourse filing that its net income rose by a limited 2% y/y to TRY2bn in 2018.

On February 21, Reuters reported that initial price guidance on Turk Telekom’s 6-year Eurobond issue stood at 7.375%. On February 14, Turkey’s largest telco said that its high-level management would carry out investor meetings arranged by mandated lenders Bank of America Merrill Lynch, Citi, ING, MUFG and Societe Generale in London, Boston and New York, starting from February 15 to issue $500mn worth of eurobonds with maturities between 5 and 7 years.

Currency rally running out of steam

The Russian investment bank expects a gradual weakening in Turkish lira toward 6.5 against USD by end-2019. The latest central bank survey predicted Turkish lira to stand at 6.2 against USD at end-2019 while Bloomberg consensus stands at 6.1.

On February 19, Jason Tuvey of Capital Economics said in a research note: “The improvement in Turkey’s current account position means the lira no longer looks fundamentally misaligned, but the recent period of stability won’t last. While a repeat of last year’s currency crisis is unlikely, the lira will depreciate and it remains susceptible to a fresh bout of global risk aversion. This is a key reason why we think that interest rates won’t be lowered as far as the markets are pricing in.”

VTB also does not expect a major lira sell-off like in August 2018. However, it expects geopolitical tension to increase further in 2019.

HSBC Holdings Plc earned about $120mn in a single day during Turkey’s financial crisis in August as it profited from the collapse of the lira, Bloomberg reported on February 19. However, lira’s collapse over the summer hit trading profits at some investment banks with exposure to the country, such as Barclays Plc.

Capital Economics expects the lira to weaken to 6.25 against USD by end-2019. This primarily reflects the large inflation differential between Turkey and the US, which means the nominal exchange rate needs to weaken to prevent the real exchange rate from appreciating.

Macro backdrop continues to improve

The stock market and currency recovery rally may be running out of steam, but Turkey’s fundamental growth story remains in place and the economy continues its surprisingly fast recovery.

VTB cut its GDP contraction forecast for 2019 to 3% from a previous 4% due to more dovish global outlook. It expects a budget deficit of 4.6% of GDP in 2019.

VTB Capital expects inflation to ease to 14.5% by end-2019. However, as interest rates have already fallen since the highs in 3Q18, and the investment bank sees from 2Q19 onwards, pressure on the lira and interest rates might escalate. VTB believes falling inflation and interest rates throughout this year have already priced in.

Annual food inflation in Turkey will likely be slower in February than in the previous month after state-run stalls in large cities opened last week, an unnamed Turkish official familiar with the figures told Bloomberg on February 20.

Total FX deposits at Turkish lenders reached $200bn as of February 15 while the central bank’s gross FX reserves slightly declined to $98.6bn, the central bank data showed on February 21.

On February 20, TUIK said that Turkish consumer confidence fell to 57.8 in February. Turks’ confidence fell to 59.9 in September and it remained close to the lowest level seen in October since then.

Based on VTB’s future inflation forecast, the current real interest rate for Turkey is some 3% and it is in line with the correlation implied by the current US 10-year yields.

VTB expects the central bank to eventually start cutting policy rates, likely after March 31 local polls, and to cut an overall 500bp at least by end-2019.

Capital Economics expects the benchmark one-week repo rate to be lowered from 24.00% now to 20.00% by end-2019, whereas the markets have pencilled in a total of around 600bp of cuts by year-end.

The average Turkish man on the street has been switching to FX from TRY since September, while corporates stopped reducing FX deposits, Tuzun also noted, adding that there has been over $20bn deposit outflow from the banking system since the currency crisis in July-August, mostly due to corporates paying back FX-debt.

Share of FX deposits at Turkish lenders climbed to 13-year high so far this year, Bloomberg reported on February 20.

On a 12-month sum basis, Turkey’s current account deficit has narrowed from as much as 6.5% of GDP in mid-2018 to 3.6% of GDP in December, according to Tuvey’s calculations. Capital Economics thinks that Turkey will post a small surplus this year – there is a whopping $175bn (22% of GDP) of external debt that needs to be serviced over the next twelve months. More than half of this debt lies in the banking sector, a legacy of the past decade’s credit boom. The upshot is that Turkey’s external financing needs are still extremely high relative to the size of its FX reserves.

The improvement in sentiment towards EMs at the start of 2018 was accompanied by a pick-up in capital flows in January, Liam Carson of Capital Economics said on February 14 in a research note, adding: “It looks like this was concentrated in flows to EM bond and equity markets, and timely figures suggest that this trend continued in early February.”

Source: Intelli News